Remember opening grandma’s birthday card as a kid and a crisp $10 note dropped out?

The super co-contribution is bit like the adult version of that.

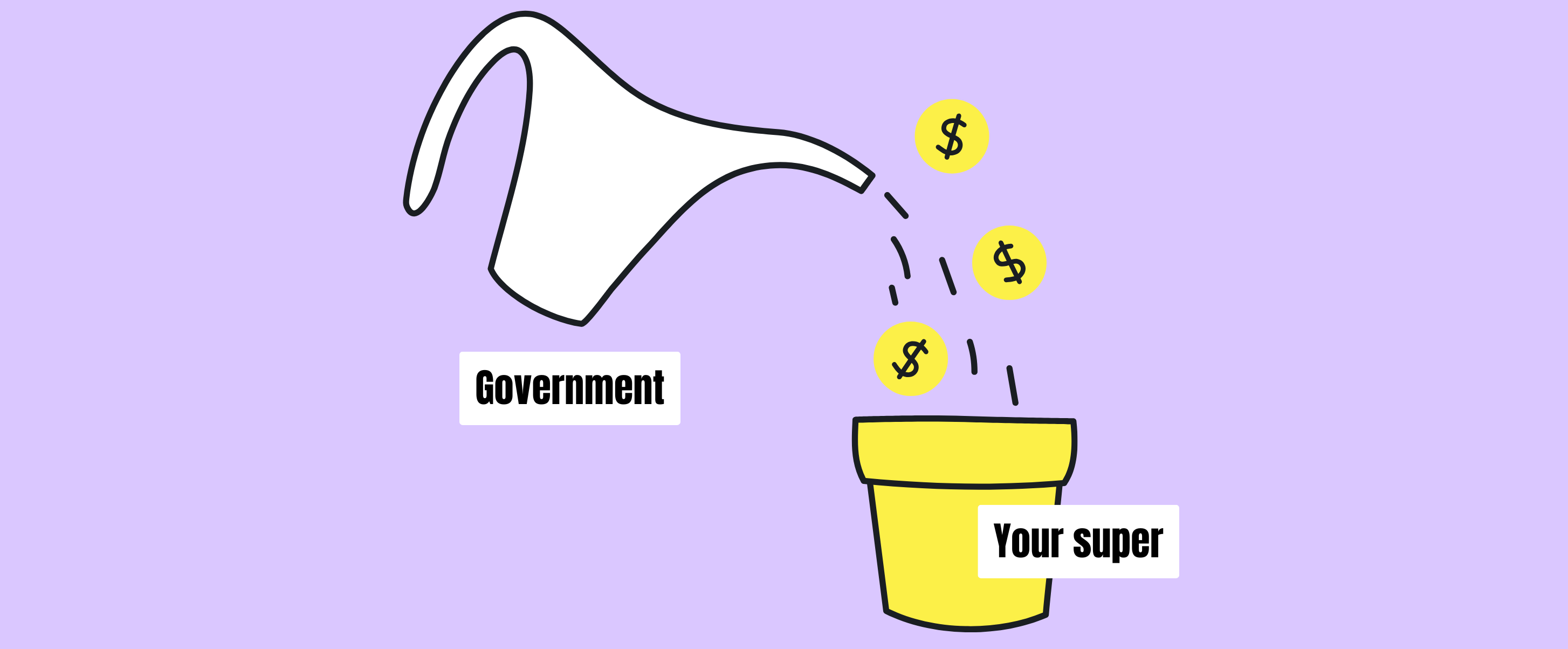

It’s a small, quiet top-up for lower-income earners who put a bit of their own money into super. Nothing life-changing, but a very tidy $500 a year on offer. And yes, plenty of people actually miss out because they have no idea it exists.

Here’s the plain-English version so you know exactly when it applies. 👇

If you make a personal, after-tax contribution (non concessional) into your super fund and your income is below a certain threshold, the government may add a bonus amount up to $500 per year. And in a move that’s very unlike the ATO, you don’t have to fill out a bagillion forms to get it. They just calculate it automatically when you lodge your tax return.

Future You gets a quiet little cheer.

You may get the co-contribution if:

✅ Your total income is under the upper threshold (total income includes reportable fringe benefits and reportable super)

✅ You make a personal non-concessional (after-tax) super contribution

✅ At least 10 percent of your income comes from a job or self-employment

✅ You lodge a tax return

✅ You’re under 71 at the end of the financial year

✅ Your total super balance at the start of the financial year is under the transfer balance cap (currently $2m)

✅ You haven’t gone over your non-concessional contribution cap (currently $120k per year)

If you tick all those boxes, you’re in the running.

Here’s the quick summary for 2025–26.

Total Income: $47,488 or less

What You Get: Up to $500. The government matches 50c for every dollar you contribute.

Total Income: $47,488 – $62,488

What You Get: You may still get something, but it reduces as your income rises.

Total Income: $62,488 or more

What You Get: You’re not eligible.

Say you earn $42,000 and you put $1000 into your super from your personal savings.

The government will kick in the full $500.

If you only put in $400, they’ll chip in $200.

Easy.

It’s free money from the government. You just need to know it exists.

And even if you’re personally above the threshold, this is great information for:

👉 Junior staff

👉 Apprentices

👉 Uni students working part-time

👉 Your kids who’ve just started earning proper money

👉 Anyone earning under sixty-odd grand

The government co-contribution won’t buy you a boat, but it’s free cash from the government and will quietly build someone’s retirement balance without costing much upfront.

If you’ve got people in your world who fall under the threshold, pass this on.

Future Them will thank you.

– The team at PAL (making accounting slightly less boring since way back when)

Disclaimer: This article is here to give you general info only, not professional advice specific to your unique situation. While efforts are made to ensure accuracy, the content may change over time. We can’t take responsibility for any decisions based on the contents of this article, so be sure to chat with your accountant or advisor first!

.jpg)

.jpg)

.png)